2026-07-14T18:30:00.000Z

Jun 12, 2026 Blog

Salesforce closed more than 22,000 Agentforce deals in Q4 FY2026 and processed 771 million Agentic Work Units, a 57% increase quarter-over-quarter. That is a deployment velocity figure that would qualify as exceptional for any enterprise software category. For a product introduced 18 months earlier, it is something else entirely.

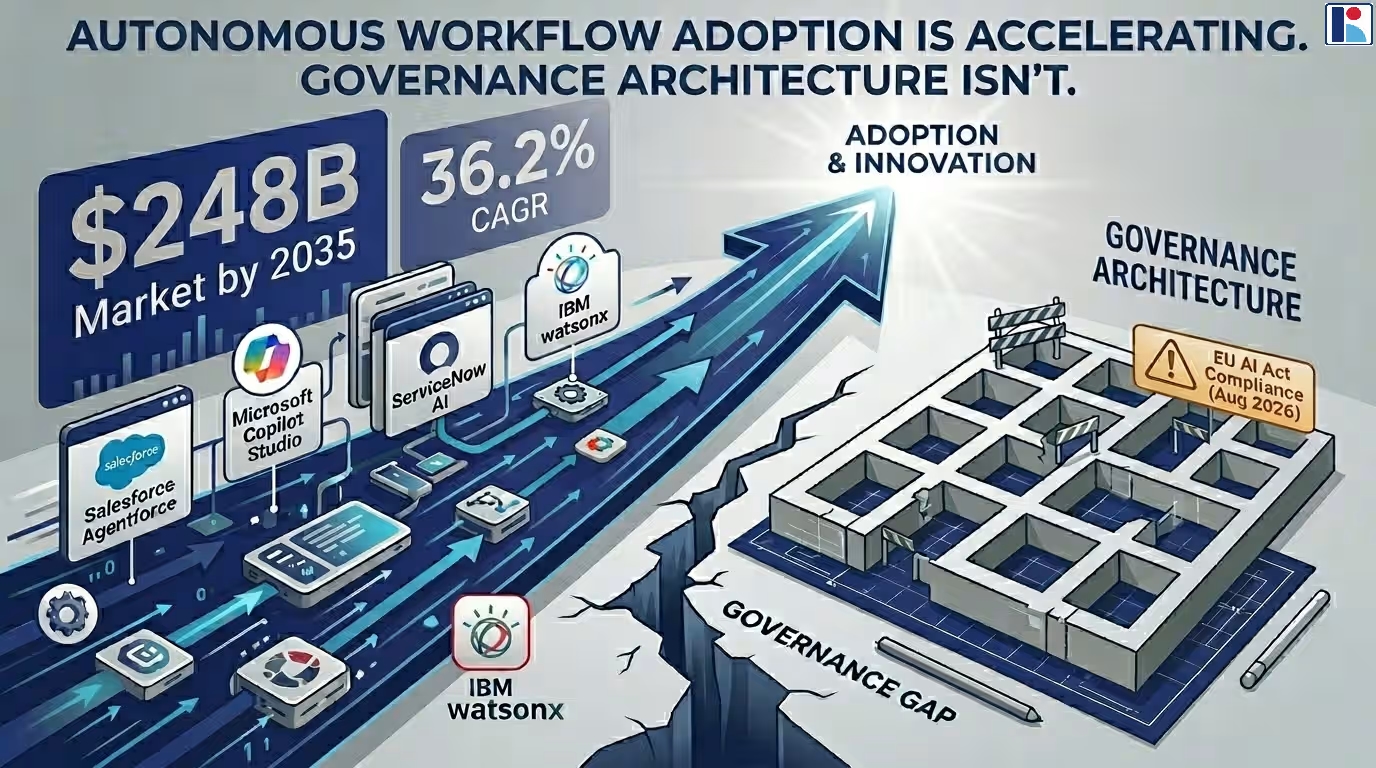

Kaiso Research's primary dataset puts the global autonomous workflow market at USD 11.5 billion in 2025. By 2035, that figure reaches USD 248.0 billion. The 36.2% CAGR is not a projection built on optimism about future capability. It is a projection built on a deployment wave that is already underway and on a set of structural forces that have not yet reached their peak.

The problem sitting inside those numbers is one that Salesforce's own 2026 Connectivity Report surfaces clearly: enterprises running an average of 12 AI agents today project that number to climb 67% within two years. Half of those agents currently operate in isolated silos, not as part of coordinated multi-agent systems. And 86% of IT leaders surveyed say they are concerned agents will introduce more complexity than value without proper integration.

That concern is well-founded. The transition from proof-of-concept to production deployment is straightforward. The transition from production deployment to governed, coordinated, multi-agent operation at enterprise scale is not.

It requires architectural decisions that most enterprises have not made, organizational capabilities that most have not built, and compliance documentation that August 2026 now makes legally mandatory in high-risk categories across the EU. Software component leads revenue across the Kaiso dataset, anchored by workflow orchestration platforms and agentic AI enterprise deployments. Cloud deployment dominates adoption architecture.

The market is not growing in spite of that tension. It is growing straight through it. The enterprises that come out ahead are the ones that treat governance architecture as a precondition of deployment, not a follow-on project.

Kaiso Research's primary dataset identifies three structural conditions that had to converge before the autonomous workflow market could reach commercial scale.

Model reliability crossed a production threshold. Between 2023 and 2025, frontier models from OpenAI, Anthropic, and Google reached the accuracy and consistency benchmarks that enterprise risk functions require before putting AI agents on consequential processes. Not laboratory benchmarks, production reliability on tasks like invoice exception handling, compliance log updates, and multi-system data reconciliation. The IBM Institute for Business Value found that AI-enabled workloads are expected to rise from 3% of enterprise volume in 2024 to 25% by 2026, an eightfold increase driven directly by that threshold crossing.

Orchestration infrastructure became available at enterprise scale. Salesforce Agentforce, Microsoft Copilot Studio, IBM watsonx Orchestrate, and ServiceNow AI Agents each delivered the coordination layer that connects LLM reasoning to live enterprise data estates. Without that layer, AI has intelligence but no operational traction. With it, agents can read CRM records, trigger ERP transactions, update compliance logs, and escalate to human reviewers in sequence, without a human initiating each step.

Enterprise procurement shifted from pilot to production. The experimentation phase that dominated 2023 and 2024 has given way to operational deployment at scale, with software-led orchestration platforms and cloud-native agentic deployments anchoring revenue across the Kaiso dataset. BFSI is moving fastest, driven by the volume and compliance structure of financial services workflows. That maturity gap between BFSI and every other vertical is not closing quickly.

The competitive structure of the autonomous workflow market in 2026 does not reward the platform with the best underlying model. It rewards the platform that controls the orchestration layer through which agents access enterprise data. That is a different competitive axis, and it explains why four platforms with very different strengths are all winning in their respective contexts.

Salesforce Agentforce now serves 18,500 enterprise customers, up from 12,500 the prior quarter, with those customers collectively running over three billion automated workflows monthly. The Agentforce 360 platform, which reached general availability in February 2026, resolves 85% of customer queries without human involvement across deployments in 124 countries. The competitive advantage is data access: Agentforce operates natively on Salesforce's CRM data model, inheriting the permission structures and audit architecture that enterprises have spent years building.

Reddit's deployment deflected 46% of support cases and cut average resolution time from 8.9 minutes to 1.4 minutes. That kind of outcome is only achievable when the agent has clean access to the underlying data.

Microsoft Copilot Studio competes on integration breadth. The 2026 Release Wave 1 introduced autonomous multi-step workflows that span Microsoft 365, Exchange, Teams, and third-party systems through Model Context Protocol connectors. The Work IQ memory layer maintains persistent context across the M365 estate, understanding job roles, project history, and communication patterns in ways that individual agents cannot.

Microsoft Entra Agent ID provides identity and access management for every agent in the stack. The bet is that enterprises already invested in Microsoft infrastructure will not build autonomous workflow architecture on a separate control plane.

ServiceNow earned the number one ranking in Gartner's 2025 Critical Capabilities report for building and managing AI agents, a position grounded in its governance-first architecture. The Now on Now deployment, ServiceNow running its own platform internally, reported $10 million in operational benefits within 120 days, equivalent to 50 full-time employees in productivity gains. ServiceNow AI Agent Orchestrator coordinates specialized agents across ITSM, HR, and customer service workflows, all built on top of thousands of pre-existing workflow templates. The limitation is entry complexity: the platform requires a dedicated administrator role before deployment begins, reflecting enterprise-grade depth that comes with enterprise-grade setup requirements.

IBM watsonx Orchestrate occupies the regulated-industry position. Pre-integrated with over 80 enterprise applications including SAP, Oracle, Workday, and Salesforce, and explicitly supporting orchestration across CrewAI, LangGraph, and IBM Bee open-source frameworks, it functions as a multi-agent supervisor for the full enterprise stack. Honda's deployment of watsonx to extract knowledge from engineering diagrams and presentations produced 67% faster knowledge modeling and 30 to 50% savings on development and planning time. For BFSI, healthcare, and government, IBM's auditability and compliance depth is the primary procurement driver, not feature breadth.

The consolidation prediction: by 2028, most large enterprises will standardize on two autonomous workflow control planes. One for customer-facing processes. One for employee-facing and back-office operations. The window for independent orchestration platforms without deep data model integrations is closing.

The Kaiso Research forecast of 36.2% through 2035 is not a straight-line extrapolation from current deployment rates. It reflects the compounding effect of three forces that individually are powerful and together are structural.

Agentic AI is the fastest-growing segment in the Kaiso dataset. The transition from single-agent deployments to coordinated multi-agent systems, where specialized agents in finance, compliance, and supply chain collaborate autonomously on complex cross-functional workflows, is the source of compounding return on autonomous workflow investment. McKinsey's 2025 State of AI survey found that 88% of organizations are using AI in at least one business function. Only one-third have begun scaling across the enterprise. That scaling transition, from functional deployment to enterprise-wide coordination, will dominate the 2026 to 2028 market cycle and produces geometric rather than linear productivity returns.

Large enterprises are the leading size segment, and their spending is accelerating. Complex multi-system workflow orchestration requires dedicated AI operations teams, cross-platform integration investment, and governance infrastructure that small and medium enterprises cannot yet absorb at the same rate. The Salesforce 2026 Connectivity Report found that enterprise application counts grew from 897 to 957 year-on-year, with only 27% of them integrated. Autonomous workflow platforms that solve the integration problem for large, fragmented data estates command premium pricing and sustained expansion revenue.

Asia-Pacific sustains the fastest consumption growth. North America anchors the highest-value enterprise procurement. Asia-Pacific, through digital transformation investment that is in earlier-stage deployment today, sustains the fastest regional growth rate across the Kaiso forecast period. Manufacturing automation in Southeast Asia, BFSI modernization in India, and government digitalization programs across the region create a demand base that is structurally different from the CRM-replacement and back-office automation use cases that drove North American adoption.

Four technology decisions determine whether an autonomous workflow deployment produces the operational outcomes in the case studies above or produces a new category of enterprise incident.

Orchestration framework selection. The choice between LangGraph for complex stateful workflows, AutoGen from Microsoft Research for multi-agent conversational coordination, and IBM Bee for open-source agent networks is not a preference question. It is an architecture question. LangGraph's graph-based state management handles conditional logic and long-running workflows that linear chain frameworks cannot support. AutoGen's conversation-driven model suits processes where agents need to negotiate decisions. Misalignment between framework and workflow type produces agent behavior that is technically correct at each individual step and operationally destructive across the full sequence.

Process context and grounding. Autonomous agents without live process context make confident decisions on stale data. Celonis and IBM Process Mining, both integrated with major orchestration platforms, provide the real-time process topology that agents need to understand transaction state, exception rules, and downstream consequences. Agents operating without this layer produce correct individual actions that create downstream process failures at a rate that becomes visible only after scale.

Governance and human-in-the-loop architecture. The EU AI Act's high-risk system requirements take full effect on August 2, 2026. Autonomous workflow deployments in BFSI, healthcare, employment, and credit decisioning that operate without documented human oversight protocols are in enforcement exposure now. The Copilot Studio 2026 Release Wave 1 human supervision trigger, which pauses execution and emails a designated user when an agent encounters ambiguity, is an architectural response to this requirement, not a product feature. Governance platforms including Modulos, Credo AI, Holistic AI, and Trustible have emerged as the compliance infrastructure layer above and across the orchestration platforms themselves.

Integration architecture and lock-in risk. Agentforce is genuinely powerful for CRM-native processes and significantly constrained for workflows touching SAP, Workday, and ServiceNow simultaneously. Copilot Studio excels inside the M365 estate and requires additional configuration for non-Microsoft systems. Enterprises treating platform selection as a single-vendor decision are building integration debt that compounds as agent counts scale. IBM watsonx Orchestrate's explicit multi-framework and multi-vendor integration architecture is the direct response to this constraint.

BFSI leads end-user revenue in the Kaiso Research dataset, and that leadership position has a structural explanation. The compliance infrastructure that financial services enterprises built over decades of GDPR, MiFID II, AML directive, and Basel III pressure maps almost directly onto the governance requirements of autonomous workflow deployment. Risk classification frameworks, human oversight triggers, audit trail requirements, and incident reporting protocols already exist. Deploying agents into that environment means configuring governance, not building it from scratch.

The workflows that BFSI has moved into autonomous operation at scale reflect this maturity. Credit decisioning support, where an agent performs the data aggregation and preliminary risk assessment and escalates boundary cases to a human underwriter. AML exception processing, where agents triage flagged transactions against typology databases and refer confirmed exceptions through established escalation chains. Customer service automation, where Agentforce deployments like the ones Salesforce reports are resolving high volumes of routine enquiries without human involvement and passing complex cases with full context to agents who can act on them.

Healthcare is where the governance tension is sharpest. The EU AI Act creates a split compliance regime: hospital workflow tools not CE-marked as medical devices face August 2026 obligations; CE-marked medical devices under MDR and IVDR face a 2027 deadline. Healthcare IT teams mapping their autonomous workflow deployments against that two-tier calendar face different timelines for adjacent systems that share data.

IBM watsonx Orchestrate's HIPAA-aligned governance architecture and audit trail infrastructure are the compliance answer for this segment. The procurement decision is not which platform has the best natural language processing. It is which platform's audit trail survives regulatory review.

Manufacturing is where multi-agent coordination delivers the most measurable operational returns. Supply chain management, procurement exception handling, IT operations monitoring, and compliance reporting each represent distinct agent deployment candidates. The compounding effect emerges when agents managing supplier invoice exceptions communicate automatically with agents tracking warehouse inventory and those monitoring logistics status, closing multi-step resolution cycles without human coordination at each handoff. UiPath's computer-use capabilities, which allow agents to operate legacy Manufacturing Execution System interfaces without API access, extend autonomous workflow into the brownfield infrastructure that most manufacturers are not replacing any time soon.

A 36.2% CAGR is real. It does not make the risks inside it disappear. Three structural risks apply across deployment contexts regardless of platform choice.

Orchestration complexity scales faster than agent capability. Adding a second agent to a workflow does not double complexity; it multiplies it. Multi-agent systems require coordination protocols, shared context management, and conflict resolution logic that adds engineering burden at each new agent. The Salesforce 2026 Connectivity Report finding that 86% of IT leaders fear agents will introduce more complexity than value without proper integration is not a confidence problem. It is an architectural observation. Organizations that treat agent deployment as a procurement exercise and not as an operational redesign produce the failure cases that slow down the enterprises deploying after them.

Error propagation in multi-agent chains is qualitatively different from single-agent errors. A procurement agent that misclassifies a supplier risk score does not just produce a wrong output. It triggers downstream agents that generate purchase orders, update compliance logs, and notify finance systems based on that misclassification. Governance architecture must define confidence thresholds that trigger human escalation before chains complete, not after.

The talent to operate agents at scale does not exist yet in most organizations. Deloitte's 2026 Agentic AI Strategy report identifies agent operations, managing agents as workers, building performance evaluation frameworks, and designing escalation protocols for autonomous systems, as the binding constraint on realized ROI for enterprises attempting autonomous workflow transformation in the 2026 to 2028 window. The enterprises deploying most successfully are treating this as an organizational capability problem, not a software configuration problem.

The August 2, 2026 EU AI Act enforcement deadline is not an abstract regulatory event. Autonomous workflow deployments in high-risk categories, credit scoring, employment processes, essential services, critical infrastructure, that lack documented risk classification, human oversight protocols, and conformity assessment frameworks are exposed to penalties reaching 40 million euros or 7% of global annual turnover. For BFSI and healthcare enterprises with European operations, the governance architecture decision needed to precede platform selection. It hasn't in most cases.

The enterprises moving fastest on remediation are not treating EU AI Act compliance as a legal workstream. They are treating it as an architectural constraint that shapes which platforms they can deploy, which workflows they can automate, and how they configure human escalation thresholds. That reframe turns a compliance deadline into a competitive design principle. Governance platforms including Credo AI, Modulos, and Trustible are receiving procurement attention not as standalone tools but as the compliance evidence layer that produces the audit trails August 2026 requires.

The procurement consolidation wave is structuring options faster than most three-year technology roadmaps anticipated. Agentforce's growth from 8,000 to 18,500 enterprise customers in two quarters and Salesforce's $1.4 billion in Agentforce and Data 360 ARR as of Q3 FY2026 signal that the evaluation period for independent orchestration platforms without incumbent stack integrations is compressing. The enterprises that defer platform selection until consolidation has occurred will negotiate from a weaker position than those that establish architecture commitments now.

That window is not closing gradually. It is closing at the same rate as the customer counts are growing.

Kaiso Research projects the global autonomous workflow market to reach USD 248.0 billion by 2035. The path there requires something that CAGR projections do not capture: a reorientation of how enterprises think about what they are building.

The organizations producing measurable returns from autonomous workflow today are not the ones that deployed the most capable agents. They are the ones that redesigned operations around agents before deploying them, defining the processes that agents would own, the thresholds at which humans would intervene, and the performance metrics that would determine whether an agent was succeeding. IBM CEO Arvind Krishna stated at IBM Think 2026 that the enterprises pulling ahead are not deploying more AI, they are redesigning how the business operates around it.

North America will anchor the highest-value enterprise procurement through platform dominance from Salesforce, Microsoft, ServiceNow, and IBM. Asia-Pacific will sustain the fastest consumption growth, driven by BFSI modernization across India, manufacturing automation in Southeast Asia, and government digitalization programs entering production deployment through 2027.

The Kaiso dataset projects agentic AI technology as the fastest-growing segment across the full forecast period. The enterprises that have been running single-agent pilots are about to discover what multi-agent coordination actually costs to govern.

The governance challenge does not diminish as the market matures. It scales with it. The enterprises that build governance architecture now are not managing a compliance problem. They are building the operational foundation that lets them move faster than their competitors when the next capability wave arrives.

The market will not wait for consensus on that point.

About Kaiso Research and Consulting

Kaiso Research and Consulting is a global market intelligence firm publishing 5,000+ research reports across 11+ industry verticals.

kaisoresearch.com | [email protected] | +1 872 219 0417

Lead Industry Analyst, Kaiso Research and Consulting | Covering AI, automation, and enterprise technology markets across North America, Europe, and Asia-Pacific

Published: 2026-06-11 | Report Code: IMEC1144

Sample Report Available at: https://www.kaisoresearch.com/report-store/global-autonomous-workflow-market/sample-request

Latest Blogs

2026-07-14T18:30:00.000Z

2026-07-08T18:30:00.000Z

2026-07-07T18:30:00.000Z