2026-07-27T18:30:00.000Z

Jun 18, 2026 Blog

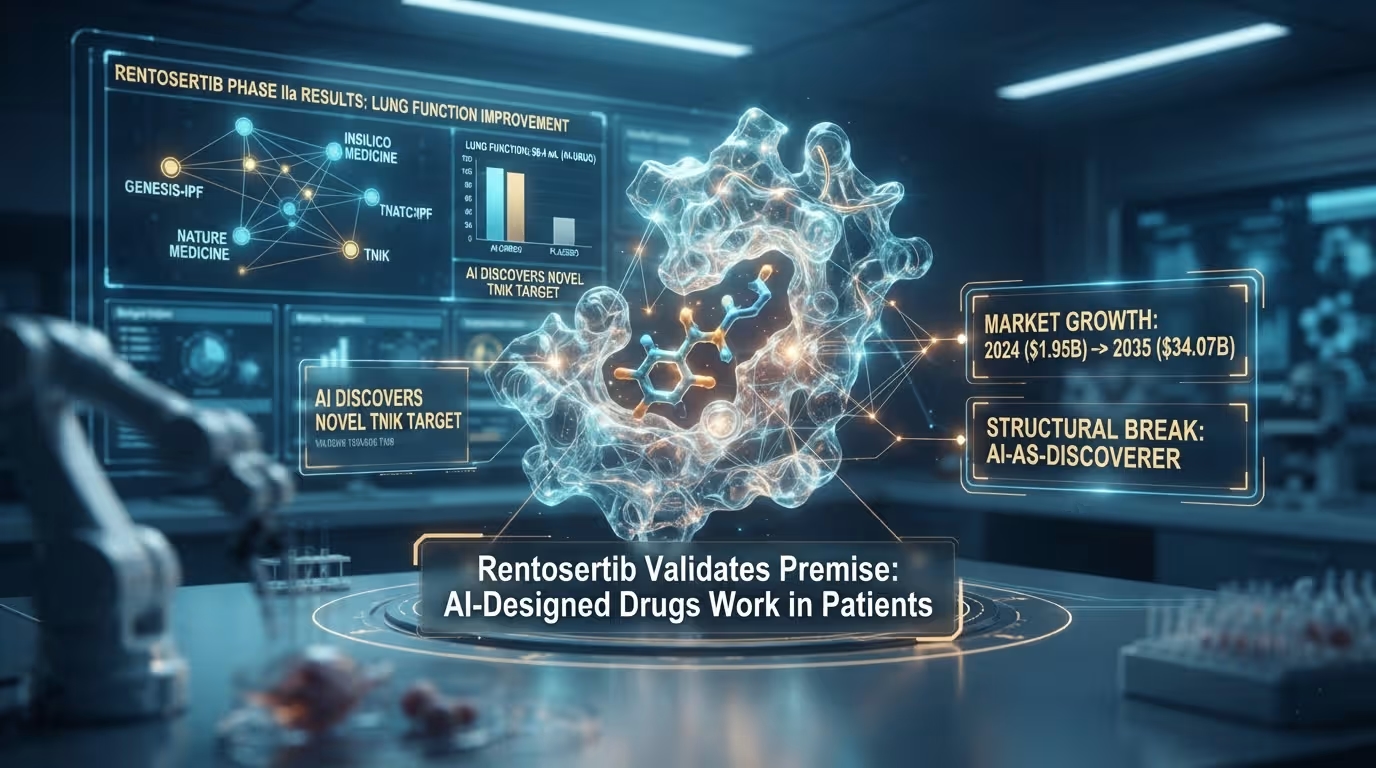

In June 2025, Insilico Medicine published Phase IIa results for Rentosertib in Nature Medicine, and the pharmaceutical industry had its first answer to a question it had been collectively avoiding: can an AI-designed drug, targeting a novel AI-identified molecular mechanism, actually work in patients? The answer, drawn from 71 patients across 22 clinical sites in China, was yes. Patients receiving 60 mg Rentosertib daily showed a mean improvement in lung function of 98.4 mL, against a mean decline of 20.3 mL in the placebo group.

That single data point did not just validate one molecule. It validated the premise that generative AI platforms can discover therapeutic targets that human biologists missed.

The question every pharma CFO should now be asking isn't whether AI-accelerated drug discovery is real. It's how many of their competitors have already committed to the infrastructure required to participate in the next wave, and how much longer a wait-and-see posture is defensible. Kaiso Research's primary dataset across this segment puts the 2024 market at USD 1.95 billion. The path to USD 34.07 billion by 2035 runs directly through the clinical validation events already in progress and the regulatory alignment events that are closing the remaining gap between AI-discovered drugs and approved market access.

This isn't a speculative growth story. The preconditions have converged.

The pharmaceutical industry adopted AI vocabulary long before it adopted AI outcomes. Between 2018 and 2023, machine learning entered drug discovery largely as a speed layer on existing workflows: faster compound screening, more efficient hit identification, better ADME prediction. What the industry got was incrementally better chemistry done faster. What it did not get was AI discovering targets that humans could not find.

That distinction matters for investors and strategists more than any revenue projection. The first generation of AI drug discovery tools operated inside human-defined chemical and biological search spaces. The current generation operates outside them. Insilico Medicine's PandaOmics engine identified TNIK (Traf2- and Nck-interacting kinase) as a druggable target in idiopathic pulmonary fibrosis through a computational scan that no traditional target identification program had prioritized.

Chemistry42, Insilico's generative chemistry engine, then designed Rentosertib's molecular structure without iterating from a known scaffold. The molecule's journey from preclinical nomination in February 2021 to Phase II initiation took under 30 months. Traditional drug development averages four or more years for the same interval.

This represents a structural break, not an incremental improvement. Kaiso Research's primary market intelligence across the AI drug discovery segment identifies this transition from AI-as-tool to AI-as-discoverer as the primary driver separating the 2024 market value from the 2035 projection.

Two additional structural factors compound the clinical validation signal. First, the Recursion Pharmaceuticals-Exscientia merger, completed in late 2024 in a USD 688 million transaction, created the industry's largest combined AI discovery platform, integrating Exscientia's generative chemistry capabilities with Recursion's phenomics data and biological profiling infrastructure. Second, Isomorphic Labs, Google DeepMind's drug discovery subsidiary, confirmed at the January 2026 World Economic Forum that its first human clinical trials for AlphaFold 3-designed oncology candidates are expected by end of 2026.

The market Kaiso Research tracks at USD 1.95 billion in 2024 is not the same market that reaches USD 34.07 billion by 2035. The intervening years contain a fundamental capability upgrade.

The case for AI's penetration of drug discovery begins and ends with a cost number that hasn't improved in 50 years. The average cost of developing a new pharmaceutical compound now exceeds USD 2 billion as of 2025, absorbing not just successful programs but the far larger volume of failed attempts. Traditional hit rates across the full discovery-to-approval pipeline remain between 10% and 20%, unchanged for decades. AI attacks the earliest and most capital-intensive parts of the attrition curve.

Multi-omics integration is the first structural driver. Machine learning algorithms operating across genomic, proteomic, and metabolomic datasets simultaneously identify hidden disease pathways that single-modality analysis cannot resolve. In oncology, where tumor heterogeneity makes uniform treatment strategies largely ineffective, this capability is central rather than marginal. The ability to decode individual patient molecular profiles and predict drug response at the biomarker level is the operational foundation of precision oncology, achievable at scale only through AI.

The second structural driver is generative molecular design. Tools like Schrödinger's FEP+ platform, Atomwise's AtomNet neural network, and deep learning models embedded in BERG LLC's and Deep Genomics' platforms now generate novel molecular structures with optimized binding and pharmacokinetics profiles before any laboratory synthesis occurs. This compresses the hit-to-lead phase from months to weeks. Atomwise's multi-year collaboration with Sanofi, announced in March 2024 with a potential deal value exceeding USD 1 billion, rests explicitly on this capability.

Third: clinical trial optimization using AI-driven patient stratification. Recursion's ClinTech initiative, announced in January 2025, extends AI application from drug design into trial architecture: smarter protocol design, accelerated patient enrollment, and adaptive evidence generation. Mid-stage oncology trials historically fail more often on patient selection than on molecular efficacy. That's the problem AI stratification directly targets.

Until January 2026, the largest single risk factor in the AI drug discovery investment thesis was not scientific. It was regulatory. Pharmaceutical companies building AI-enabled discovery pipelines could not be certain that AI-generated data, AI-identified targets, or AI-designed molecular candidates would be treated by the FDA or EMA as credible inputs into IND applications.

That uncertainty resolved substantially on January 14, 2026, when the FDA and EMA published their first joint framework: ten guiding principles for good AI practice in drug development. The document explicitly addressed the conditions under which AI-generated data can support regulatory submissions and how sponsors should structure pre-IND discussions around AI tools. Separately, the FDA's 2025 draft guidance on AI credibility opened the door by inviting sponsors to discuss AI use in pre-submission meetings, signaling that the agency was treating AI-generated evidence as admissible rather than presumptively suspect.

For pharma boards, this regulatory shift does something more important than clarify submission requirements. It removes the legal uncertainty that had been suppressing capital allocation to AI-integrated discovery programs. The EU AI Act, taking full effect in August 2026, adds a compliance timeline that concentrates the capital deployment window further.

EMA had accepted exploratory AI analyses, including machine learning-derived biomarkers, in scientific advice contexts before the joint publication, provided they met transparency and validation standards. What the January 2026 document did was systematize that acceptance into a framework sponsors can build programs around. The distinction between a favorable precedent and a governing framework is not semantic when the decision involves multi-billion dollar R&D allocation.

The AI drug discovery competitive landscape has entered its consolidation phase. Kaiso Research's sector coverage across this vertical identifies three distinct competitive tiers with fundamentally different strategic positions.

The platform integrators occupy the first tier. Recursion Pharmaceuticals, following the Exscientia merger, operates a full-stack pipeline spanning patient-centric target discovery, 2D and 3D generative AI molecule design, automated chemical synthesis, and active learning design-make-test-learn cycles. The combined entity entered 2025 with more than twenty clinical and discovery programs and a stated goal of at least seven clinical readouts during the year. The USD 500 million in partnership milestones received from Roche and Sanofi through 2025 signals that large pharmaceutical companies view Recursion's platform as worth paying for in advance of product proof.

Isomorphic Labs represents a structurally different model: a Google DeepMind subsidiary with access to AlphaFold's computational architecture, pursuing oncology and immunology programs built on AlphaFold 3's molecular interaction predictions. The clinical readouts expected by end of 2026 will determine whether the Alphabet AI infrastructure advantage translates into therapeutic success at the same rate it has translated into scientific publications.

The specialized niche players form the second tier. Insilico Medicine, with Rentosertib's Phase IIa data published in Nature Medicine, established proof-of-concept that generative AI can discover novel targets and design first-in-class molecules for diseases with unmet need. BenevolentAI's partnership with AstraZeneca, expanded in October 2023 to cover chronic kidney disease and idiopathic pulmonary fibrosis, positions it as an AI target discovery engine for a major pharmaceutical pipeline.

The technology infrastructure layer is the third tier. NVIDIA Corporation's BioNeMo platform provides the GPU compute and specialized biological foundation models that most AI drug discovery pipelines depend on for large-scale molecular simulation. Microsoft Corporation's Azure Life Sciences cloud environment supports computational chemistry workflows across the sector. IBM Watson Health's capabilities in biomedical literature mining anchor the natural language processing dimension of the market.

The consolidation visible in the Recursion-Exscientia merger will not be the last structural transaction in this sector. Platforms that lack either proprietary biological data or validated AI-designed clinical candidates are increasingly exposed to acquisition or exit.

Not all therapeutic areas are equally positioned to benefit from AI drug discovery. Kaiso Research's primary dataset identifies oncology as the leading therapeutic area by adoption, venture capital concentration, and clinical pipeline density.

Oncology benefits from AI in three distinct ways that do not apply equally elsewhere. First, tumor biology produces multi-dimensional molecular data at a scale no other disease class matches. Genomic alterations, proteomic expression patterns, and immune cell infiltration profiles all vary between patients. Machine learning models trained on this data identify clinically meaningful subpopulations that traditional trial designs aggregate.

Second, oncology has the highest tolerance for accelerated regulatory pathways, including FDA Breakthrough Therapy designation and Accelerated Approval, which means AI-identified candidates can reach patients faster when early signals are compelling. Third, the oncology competitive landscape has forced pharmaceutical companies to adopt biomarker-driven trial designs, making the infrastructure for AI-stratified patient selection more developed here than anywhere else.

Neurology represents the second-highest opportunity concentration. Central nervous system drug development has historically suffered from the most severe attrition rates in all of pharmaceutical research, driven by incomplete understanding of disease mechanisms and the blood-brain barrier's resistance to most molecular scaffolds. AI's ability to mine electronic health records, imaging data, and genetic databases simultaneously to identify novel CNS targets is particularly valuable precisely because human biologists have exhausted the most obvious mechanistic hypotheses.

Metabolic and cardiovascular indications follow in the therapeutic area hierarchy. The integration of multi-omics data with real-world evidence from continuous glucose monitors and cardiac rhythm devices creates training datasets for precision medicine models that did not exist five years ago.

Machine learning retains its position as the dominant technology sub-segment within AI drug discovery. Pattern recognition across multidimensional biomedical data spaces is fundamentally a machine learning problem: finding correlations in high-dimensional input spaces that human researchers cannot perceive. Every major platform in this market, from Insilico's PandaOmics to Atomwise's AtomNet to Schrödinger's FEP+ engine, runs machine learning as its primary computational substrate.

Natural language processing is the fastest-growing technology sub-segment. The reason is not linguistic. It's the volume of unstructured scientific knowledge locked in biomedical literature, patent filings, clinical trial records, and electronic health record databases that standard computational approaches cannot access.

NLP models trained on PubMed's database of 35 million biomedical abstracts, combined with patent text and FDA submission records, can identify compound mechanisms and target-disease associations that would require decades of expert literature review to surface manually. IBM Watson Health's NLP capabilities and BenevolentAI's knowledge graph platform are both built around this exact bottleneck.

Context-aware processing is the emerging technology bet. Unlike machine learning, which finds patterns in structured data, and NLP, which extracts information from text, context-aware processing integrates heterogeneous data types into coherent analytical frameworks. It allows a platform to simultaneously process a patient's genomic sequence, their electronic health record, and the chemical properties of a candidate molecule to generate a patient-specific drug response prediction. Recursion's ClinTech framework depends on context-aware processing more than on any other technology category.

Kaiso Research's primary market data confirms that technology sub-segment leadership will shift over the 2025-2035 forecast period. Machine learning dominates today. Context-aware processing will be the defining competitive differentiator by the early 2030s.

North America's dominance in the AI drug discovery market reflects three compounding advantages: the concentration of major pharmaceutical R&D in the United States, the world's deepest venture capital network for life sciences and AI, and the largest installed base of high-performance computing infrastructure available to biotech companies. The FDA's 2025 draft guidance on AI credibility, followed by the joint FDA-EMA principles in January 2026, positioned North American regulatory infrastructure as the most explicitly welcoming environment for AI-generated pharmaceutical data submissions.

Europe's position is structurally strong but historically constrained by regulatory complexity in ways the joint principles were designed to alleviate. The UK has positioned itself as a post-Brexit hub for AI biotech, with BenevolentAI headquartered in London. Germany and Switzerland anchor the continental European pharmaceutical AI infrastructure through Roche and Novartis, both of which have committed significant capital to external AI discovery partnerships rather than purely internal platform development.

Asia-Pacific is the growth-rate story. China's government investment in AI infrastructure and life sciences, combined with a rapidly expanding computational biology talent pool, has positioned the country as the primary location for a parallel AI drug discovery industry cluster. Insilico Medicine runs its autonomous robotics laboratory in Suzhou, China, and conducted the GENESIS-IPF Phase IIa trial across 22 Chinese clinical sites.

India and South Korea are building AI biotech capacity through academic programs and government life sciences initiatives. The Asia-Pacific region will not displace North America's platform leadership within the forecast window, but it will capture a disproportionate share of the clinical trial infrastructure investment that AI drug development creates.

Venture capital concentration in AI drug discovery accelerated materially between 2023 and 2025. Global venture funding in the sector reached USD 3.3 billion in 2024. Notable anchoring transactions include Novartis partnering with Generate:Biomedicines in a USD 1 billion collaboration in 2024, and Isomorphic Labs raising more than USD 600 million for AlphaFold-integrated drug design in 2024.

The Atomwise-Sanofi collaboration, with a potential deal value exceeding USD 1 billion, represents the archetype for pharma-AI platform partnerships: upfront commitment in exchange for priority access to computational discovery infrastructure.

The deal structure characterizing this market matters as much as the deal volume. The Sanofi-Atomwise and AstraZeneca-BenevolentAI partnerships are not licensing arrangements for known compounds. They are pre-purchase agreements for future discovery output from AI platforms with demonstrated but not exhaustively proven capabilities. This signals that large pharma boardrooms have made a collective judgment: building comparable AI drug discovery capability internally is slower and more expensive than acquiring it through strategic partnership.

Healthcare investors face a portfolio construction question specific to this market. Differentiate between AI platform companies building discovery infrastructure and AI pipeline companies advancing AI-discovered compounds toward approval. The risk and return profiles differ materially. Platform companies generate revenue through partnerships before clinical validation.

Pipeline companies generate revenue only when compounds reach late-stage trials or partnerships. Both categories contain significant opportunity. They do not belong in the same risk bucket.

Three structural risks shadow the growth trajectory.

Data quality and interoperability remain the primary operational constraint. Electronic health records across health systems are not standardized. Genomic databases collected under different consent frameworks and sequenced with different technologies are not readily combinable.

The AI platforms that have achieved clinical output, including Insilico, Recursion, and BenevolentAI, have addressed this through proprietary data collection programs and controlled-access partnerships with health systems and CROs. Mid-tier companies that lack these data relationships face a capability gap no algorithmic sophistication can bridge.

The talent constraint is real and narrow. Building AI drug discovery capability requires professionals who understand both computational science and molecular biology at a depth that neither field's traditional training produces. The overlap between AI research talent, computational chemistry expertise, and biological domain knowledge is small globally, geographically concentrated in the clusters where competing platforms already operate, and expensive. This constraint will not resolve within the 2025-2035 forecast window without deliberate investment in interdisciplinary graduate training by research universities in the U.S., UK, China, and India.

Regulatory harmonization is better than it was in January 2026 but it is not complete. The FDA-EMA joint principles provide a framework. They do not provide pre-approved submission templates or confirmed parity between AI-generated and conventionally generated preclinical data across all regulatory jurisdictions. Companies with Asia-Pacific regulatory submissions in mind face PMDA requirements in Japan and CDSCO requirements in India that have not published comparable AI data acceptance frameworks.

Rentosertib's Phase IIa publication in Nature Medicine in June 2025 was the most important commercial signal in this market since Insilico Medicine nominated the compound as a preclinical candidate in 2021. Not because one drug in one indication validates a USD 34 billion market projection. Because it answered, for the first time in this industry's history with AI, the foundational question: can a generative AI platform discover a target that human biology missed, design a molecule for that target from scratch, and produce clinical results that justify further development? The answer was yes.

Kaiso Research's primary dataset across this segment tracks the 2024-to-2035 compound annual growth rate at 29.7%, a figure that reflects not optimism about what AI might eventually do for pharmaceutical R&D, but evidence about what it's already doing. The companies that treated the Rentosertib result as confirmation rather than as news have been building infrastructure since 2021.

The pharmaceutical industry's attrition model is broken. AI won't repair it. AI will replace it.

---

About Kaiso Research and Consulting

Kaiso Research and Consulting is a global market intelligence firm publishing comprehensive research reports across key industry verticals.

Latest Blogs

2026-07-27T18:30:00.000Z

2026-07-14T18:30:00.000Z

2026-07-08T18:30:00.000Z